As a business owner, are you doing everything legally possible to minimize your tax liability and ensure you’re only paying your fair share—not a penny more?

As the saying goes, it’s not what you make, but what you keep. Choosing the right structure for your business, such as an LLC (Limited Liability Company) or an S-Corporation (S-Corp), can significantly impact your federal tax obligations. While both entities offer liability protection, they differ in how your business income is taxed, which can affect your overall tax burden. By understanding the key differences between these structures, you can make an informed decision that aligns with your financial goals.

LLC Overview

An LLC is a flexible business structure that offers liability protection to its owners (referred to as “members”) while allowing them to choose how they want to be taxed. By default, the IRS taxes a single-member LLC (one owner) as a sole proprietorship and a multi-member LLC (more than one owner) as a partnership. However, LLCs can also elect to be taxed as a C-Corporation or S-Corporation.

S-Corporation Overview

An S-Corporation (S-Corp) is not a separate business entity but rather a special tax election available to LLCs or corporations. Electing S-Corp status allows business owners to avoid double taxation and reduce the self-employment taxes typically applicable to LLC owners. Like LLCs, S-Corps are pass-through entities, meaning business income passes through to the owners and is taxed at the individual level rather than the corporate level.

In this article, we’ll explore the federal tax implications of LLCs and S-Corps, breaking down the benefits and challenges of each structure to help you decide which is right for your business.

Case Study: ACB Business – LLC vs. S-Corp Taxation

Let’s use a scenario to illustrate the tax differences between LLC and S-Corp elections:

- Business: ACB Business, a single-member LLC owned by James Matrix

- 2023 Net Profit: $250,000

- S-Corp Election: James pays himself a $150,000 salary in line with S-Corp requirements

How James is Taxed as an LLC

As a single-member LLC, ACB Business is considered a disregarded entity for tax purposes. This means the business’s profits and losses are reported on James’s personal tax return (Form 1040) via Schedule C. James is responsible for paying self-employment taxes on the net business income.

- Self-Employment Tax: The IRS requires LLC owners to pay self-employment taxes, which cover Social Security and Medicare contributions. This tax is set at 15.3% (12.4% for Social Security and 2.9% for Medicare) and applies to net earnings from self-employment.

- Federal Income Tax: In addition to self-employment taxes, James is subject to federal income tax based on his personal tax bracket, which ranges from 10% to 37%.

How James is Taxed as an S-Corp

If ACB Business elects to be taxed as an S-Corporation, the primary tax-saving opportunity comes from reducing self-employment taxes. As an S-Corp owner, James is required to pay himself a reasonable salary, which will be subject to employment taxes (Social Security and Medicare). The remaining business profit can be distributed as dividends, which are not subject to self-employment taxes.

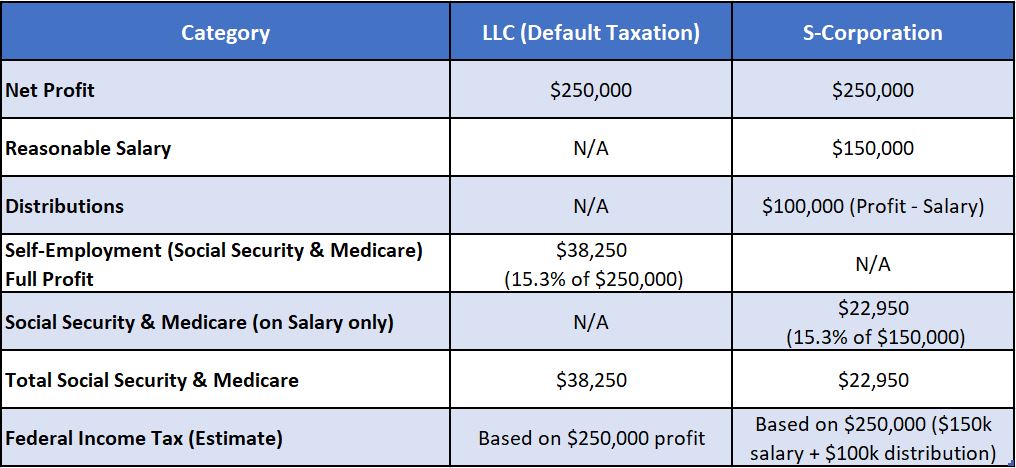

Side-by-Side Comparison: LLC vs. S-Corp Tax Implications

Federal Tax Implications Explained

1. LLC (Default Taxation):

- Under default LLC taxation, the full $250,000 profit is subject to self-employment taxes, resulting in $38,250 in Social Security and Medicare taxes.

- Additionally, federal income tax is owed based on individual tax brackets. Assuming an effective tax rate of 24%, this would equate to approximately $60,000 in federal income tax.

- Total tax liability: $38,250 (self-employment tax) + $60,000 (income tax) = $98,250.

2. S-Corporation:

- As an S-Corp, James only pays employment taxes on his $150,000 salary, which results in $22,950 in Social Security and Medicare taxes. The remaining $100,000 in profit is distributed as dividends, which are not subject to self-employment tax.

- The total $250,000 (salary + distribution) is still subject to federal income tax, leading to the same estimated $60,000 federal income tax liability.

- Total tax liability: $22,950 (employment tax) + $60,000 (income tax) = $82,950.

Total Tax Savings with an S-Corp

By electing S-Corp status, James could reduce his total tax liability by $15,300 ($98,250 – $82,950). This savings stems from paying self-employment taxes only on his reasonable salary rather than the entire business profit.

Additional Considerations

While S-Corp taxation offers notable tax savings, certain requirements must be met in order to be able to make the S-Corporation election and it also comes with added responsibilities:

- Reasonable Salary Requirement: The IRS mandates that S-Corp owners pay themselves a reasonable salary. Underpaying yourself to reduce taxes can lead to penalties.

- Payroll and Reporting: As an S-Corp owner, you must run payroll for yourself and file quarterly payroll tax returns (Forms 941 and 940).

- Corporate Formalities: S-Corps must adhere to certain formalities, including holding shareholder meetings, maintaining minutes, and complying with other regulatory requirements.

Conclusion

For ACB Business, electing S-Corp status could result in substantial tax savings by reducing the income subject to self-employment taxes. However, it’s important to weigh these savings against the additional administrative responsibilities of operating an S-Corp.

Before making any changes to your business structure, it’s wise to consult with a CPA or tax professional. They can assess your specific situation and ensure the S-Corp election aligns with your business’s financial goals. Understanding the federal tax implications of each structure will help you make a decision that optimizes your tax savings while keeping your business compliant.